VIX & VIX Futures Term structure

VIX、VIX 期貨期限結構

What is VIX Volatility Index?

VIX is the ‘implied’ 30-day volatility of the S&P 500 derived from call and put options. It represents the probable range of movement in the S&P 500 above and below its current level in the immediate future.

For example, if VIX is 20 now, take VIX divided by square root of 12. The number 20 can be interpreted as that over the next 30 days, there is a 68% chance ( 1 standard deviation) that the S&P 500 will be trading within the range of +/-5.77% (equivalent to +/-20% annualized).

何為 VIX 波動率指數?

VIX 是由 S&P 500 的 30 天看漲、看跌期權推算出來的波動率,代表 S&P 500 未來 30 天內可能上漲或下跌的範圍。

舉例來說,如果現在 VIX 為 20,代表 S&P 500 有 68% 的機率 (一個標準差),未來一個月的漲、跌範圍在 20/Sqrt(12) = 5.77%,因為 VIX 為年化後的數字,所以必需除以根號 12,將之轉成一個月的結果。

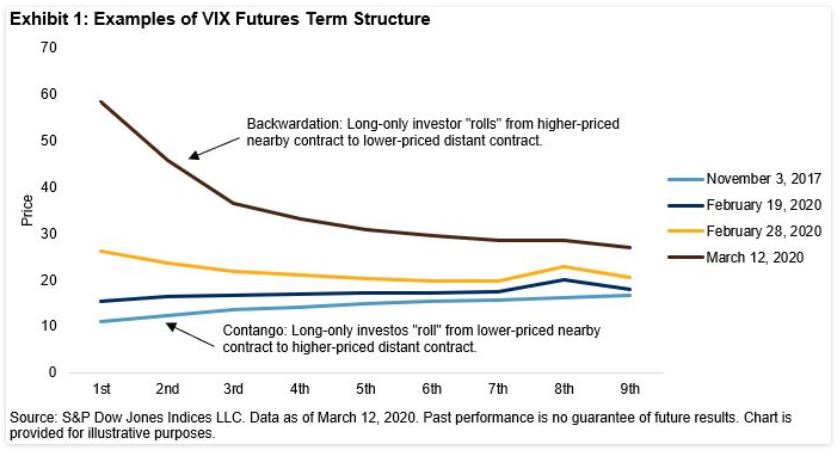

What is VIX futures term structure?

VIX term structure is the relationship between VIX futures prices and maturity dates. It is said to be in Contango when VIX futures are priced higher than the VIX spot and in Backwardation when the relationship is reversed. For both Contango and Backwardation, the term structure curve can also take the shape of either concave up or concave down, depends on whether the mid-term futures prices are closer to the short-term prices or to the long-term prices.

何為 VIX 波動率期限結構?

VIX Futures Term Structure 是 VIX 期貨價格、到期時間的關係圖,如果 VIX 遠期指數高於 VIX 現貨指數、稱之為 Contango 期貨溢價,反之則稱為 Backwardation。

通常期限結構是 Contango、向上傾斜,代表到期日較長的 VIX 期貨價格高於短期價格,但曲線形狀會隨市場對波動性預期的變化而改變。

取決於 VIX 中期指數高低,Contango、Backwardation 情況下,曲線都可能出現上凸 (concave up) 或下凹 (concave down) 的情形。

VIX 期限結構可以幫助投資人洞察市場未來波動水平,以及構建可盈利的交易策略,例如若投資人預期短期波動性會上升,短期 VIX 期貨合約價格上漲速度會快於 VIX 長期合約價格,曲線形成 Backwardation 情況。

|

| Source: spglobal.com |

Why VIX Future Term Structure is important?

The VIX futures term structure is important for investors who want to gain insights into market expectations for future levels of volatility. Here are some of the key reasons:

- Market Sentiment

- The shape of the VIX futures term structure can provide information about market sentiment towards future levels of volatility. A steeply upward sloping term structure indicates that market participants expect higher levels of volatility in the near term, while a flat or downward sloping term structure suggests that volatility is expected to remain relatively stable or decline

- Risk Management

- The VIX futures term structure can be used by investors as a risk management tool. For example, if an investor is concerned about a potential increase in market volatility, they may purchase VIX futures contracts with longer expiration dates, which tend to be more sensitive to changes in the VIX. This can help to protect their portfolio against losses in the event of a market downturn

- Trading Strategies

- The shape of the VIX futures term structure can also be used as a basis for trading strategies. For example, a trader may use the term structure to identify opportunities for "roll yield," which involves buying VIX futures contracts with shorter expiration dates and selling contracts with longer expiration dates. This strategy can be profitable if the term structure is upward sloping and volatility expectations are met or exceeded.

Overall, the VIX futures term structure provides valuable information about market expectations for future levels of volatility, which can be used by investors and traders to manage risk and develop trading strategies.

VIX Term Structure 的重要性

VIX 期貨期限結構是希望深入了解市場對未來波動水平預期的投資人重要的工具,以下是一些關鍵原因:

- 市場情緒

- VIX 期貨期限結構的形狀,能提供市場情緒對未來波動率的信息,陡峭向上傾斜的期限結構代表市場預計短期內有更高的波動,而平坦或向下傾斜的期限結構表明波動率將保持相對穩定或下降

- 風險管理

- VIX 期貨期限結構可供投資人風險管理工具,例如,若投資擔心市場波動性可能增加,可能購買到期日較長的 VIX 期貨合約,因這些合約對 VIX 變化更為敏感,有助於保護他們的投資組合在市場低迷時的損失

- 交易策略

- VIX 期貨期限結構的形狀可以用作交易策略的基礎,例如,投資人可以使用期限結構來識別“滾動收益率”的機會,購買到期日較短的 VIX 期貨合約、賣出到期日較長的合約。 如果期限結構向上傾斜並且達到、或超過波動率預期,則策略可以盈利

How to Check VIX Futures Term Structure|如何查詢 VIX 期貨期限結構

Website to check VIX futures term structure: http://vixcentral.com/

Two Kinds of Volatility 兩種波動率

- 歷史波動率 Historical Volatility HV

- 自收益率數據中計算得出,反映過去和現在的波動率狀況

- 隱含波動率 Implied Volatility IV

- 從期權數據中計算得出,反映投資人對於未來價格波動的預期

結 語

CBOE的波動率指數 VIX 是衡量市場波動性的重要指標,VIX 呈現的是 S&P 500 指數期權價格的 30 天隱含波動率,一般被作為市場系統性風險的指標,通常情況下,短期股票的收益率與歷史波動率呈現負相關,但未來股票的收益率則與隱含波動率呈現正相關。

VIX 期貨期限結構 VIX Futures Term Structure 則提供市場對未來波動率預期的重要訊息,投資人可用來管理風險和制定交易策略。

{kind=link}

0 comments